The Evolution of Efficiency: Navigating Modern Commercial Loan Origination Software

In the rapidly shifting landscape of global finance, the ability to process complex lending requests with both speed and precision has become the ultimate competitive advantage. For decades, the commercial lending sector was defined by mountainous paperwork, fragmented spreadsheets, and long, opaque approval cycles that frustrated both lenders and borrowers. However, the rise of sophisticated commercial loan origination software has fundamentally rewritten the rules of the game. This technology acts as the digital backbone of modern financial institutions, transforming a traditionally cumbersome manual process into a streamlined, data-driven journey. By integrating automated workflows, real-time risk assessment, and centralized document management, these platforms allow banks and credit unions to move from application to funding with unprecedented agility.

The true value of a robust commercial loan origination software system lies in its ability to handle the “messy” nature of commercial credit. Unlike residential mortgages, which often follow a standardized path, commercial loans involve intricate entity structures, varied collateral types, and complex financial covenants. Modern software is designed to digest this complexity, offering tools that not only capture data but also provide the analytical depth required to make sound credit decisions in a high-stakes environment. As we move further into 2026, the adoption of these systems is no longer a luxury for mid-sized or large lenders; it is a fundamental requirement for survival in a market where borrowers expect the same digital ease from their business bank that they receive from their favorite consumer apps.

Understanding the Core Framework of Loan Origination

At its simplest level, commercial loan origination software serves as a specialized project management tool tailored for the lifecycle of a business loan. It begins the moment a relationship manager enters a prospect’s details and follows the deal through every gate—underwriting, credit committee approval, document preparation, and finally, the closing table. The magic happens in the background, where the software triggers specific tasks based on the loan type or risk profile. For example, if a loan exceeds a certain dollar threshold, the system can automatically route the file to a senior credit officer, ensuring that institutional guardrails are respected without the need for manual oversight.

One of the most significant shifts in recent years is the transition from “siloed” systems to integrated ecosystems. In the past, a lender might use one program for spreading financials, another for tracking documents, and a third for generating the final loan agreement. A modern commercial loan origination software platform eliminates these gaps by providing a “single source of truth.” When data is entered once, it flows seamlessly throughout the entire lifecycle. This not only reduces the risk of human error—which is rampant when re-keying data across different screens—but also ensures that everyone from the loan assistant to the Chief Credit Officer is looking at the exact same information at the exact same time.

The Lifecycle of a Commercial Credit Facility

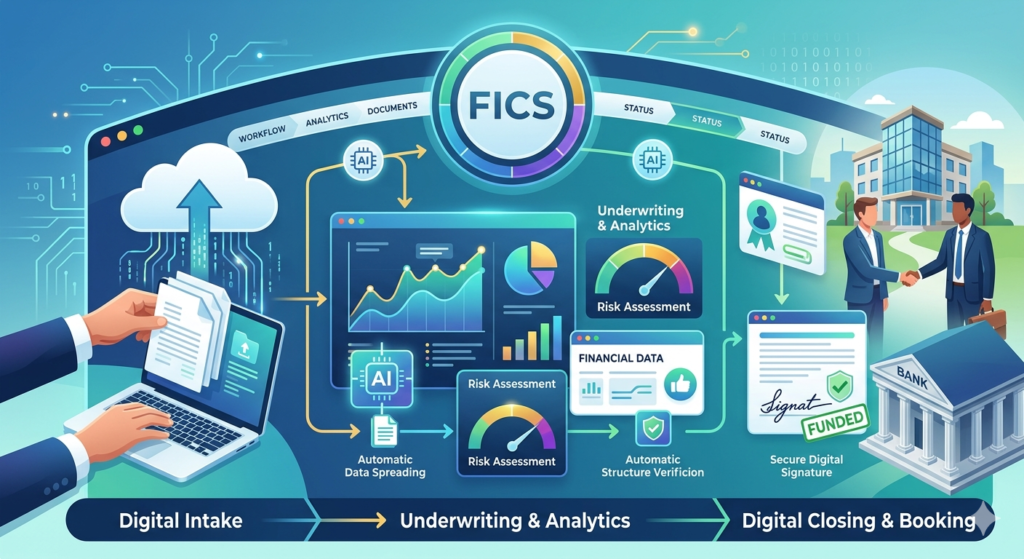

The journey through a commercial loan origination software platform typically follows a structured path designed to maximize efficiency. It starts with the “Intake” phase, where digital portals allow borrowers to upload tax returns, financial statements, and organizational charts directly into the system. From there, the “Underwriting” module takes over. Here, the software can pull automated credit reports and use optical character recognition to “read” financial documents, prepopulating spreading templates that would have previously taken an analyst hours to complete manually.

Once the credit package is built, the “Decisioning” phase begins. This is where the institution’s specific risk appetite is coded into the system. The commercial loan origination software evaluates the deal against internal policy—checking debt service coverage ratios, loan-to-value limits, and industry exposure. If the deal passes these automated checks, it moves to the “Closing” phase, where the system integrates with document generation tools to produce a consistent, compliant closing package. This end-to-end connectivity ensures that the final loan booked into the core banking system matches exactly what was approved by the credit committee.

Essential Features of High-Performing Lending Platforms

When evaluating commercial loan origination software, there are several non-negotiable features that differentiate a mediocre tool from a transformative one. Chief among these is robust document management. Commercial loans are notoriously document-heavy, requiring everything from environmental reports to complex partnership agreements. A top-tier system includes a dynamic “document checklist” that updates in real-time. If a specific collateral type like “Heavy Equipment” is selected, the software should automatically add the requirement for a UCC-1 filing and an equipment appraisal to the closer’s to-do list, ensuring nothing falls through the cracks.

Another critical element is advanced risk and compliance integration. In the current regulatory environment, the “Know Your Customer” (KYC) and Anti-Money Laundering (AML) requirements are more stringent than ever. Modern commercial loan origination software often features built-in integrations with global databases to perform these checks instantly. Furthermore, the software provides a comprehensive “audit trail,” documenting every change, comment, and approval. This level of transparency is invaluable during regulatory exams, as it allows the bank to prove exactly why a loan was approved and who authorized the various exceptions along the way.

Customization and Scalability

Every financial institution has its own unique “secret sauce”—the specific way they evaluate risk or handle customer relationships. Therefore, the best commercial loan origination software is highly configurable. It shouldn’t force a community bank to act like a global powerhouse, nor should it restrict a large entity’s ability to create complex, multi-layered approval hierarchies. Flexibility in workflow design allows institutions to mirror their existing successful processes while adding the speed of automation.

FICS: Bridging the Gap in Lending Technology

In the discussion of industry leaders, it is important to note companies like FICS that have built a reputation for providing reliable, specialized tools for lenders. While many platforms try to be everything to everyone, the most successful implementations often come from vendors who understand the specific nuances of different lending sectors. Whether it is residential or commercial servicing, having a technology partner that prioritizes data integrity and user-friendly interfaces is essential for long-term success.

The Strategic Importance of Data Analytics

Beyond just processing loans, commercial loan origination software has become a goldmine for business intelligence. By capturing thousands of data points across the lending portfolio, these systems allow executives to spot trends that were previously invisible. For instance, a bank might use the reporting engine to realize that their approval times for medical practice loans are 20% slower than for industrial real-estate, prompting a review of the underwriting criteria for that specific niche.

Predictive analytics is the next frontier for these platforms. By looking at historical data, advanced commercial loan origination software can begin to flag “at-risk” applications before an analyst even opens the file. If the system notices a pattern of defaults in a specific geographic region or industry sector, it can alert the credit team to exercise extra caution. This shift from reactive to proactive risk management is perhaps the greatest benefit of moving away from paper-based or legacy digital systems.

Common Pitfalls During Implementation

Despite the clear benefits, transitioning to a new commercial loan origination software is a significant undertaking that is fraught with potential mistakes. One of the most common errors is “paving the cow path”—simply digitizing an existing, inefficient manual process instead of using the new technology to rethink the workflow from the ground up. If your manual process has five redundant approval steps, simply moving those steps into a software environment won’t solve your speed issues. Implementation is the perfect time to perform a “process audit” and eliminate bottlenecks that no longer serve a purpose in a digital world.

Another frequent mistake is underestimating the importance of data migration. Moving active loan files from an old system to a new commercial loan origination software platform is a delicate operation. If the data is “dirty”—full of duplicates, missing fields, or incorrect formatting—those errors will be magnified in the new system. Lenders must invest the time to clean their data before the “go-live” date. Furthermore, a lack of comprehensive staff training can lead to poor adoption rates. If the relationship managers find the new system too complex or frustrating, they will find ways to work around it, defeating the purpose of the investment.

Over-Customization vs. Standard Features

Lenders often fall into the trap of wanting to customize every single screen and field within their commercial loan origination software. While some customization is necessary, “over-engineering” the platform can lead to long-term headaches. Excessive custom code can make future software updates difficult to implement and may slow down the system’s performance. The smartest approach is to stick to the “out-of-the-box” functionality as much as possible, only requesting custom builds for features that provide a genuine competitive advantage or are required for specific regulatory compliance.

Future Trends: AI and the Human Touch

As we look toward the future of commercial loan origination software, the integration of Artificial Intelligence (AI) is the most discussed trend. AI isn’t here to replace the commercial lender; rather, it is here to act as a highly efficient assistant. AI-driven “co-pilots” can now summarize hundreds of pages of legal documents in seconds, highlighting potential red flags for the human underwriter to review. This “human-in-the-loop” model ensures that while the heavy lifting of data entry and initial screening is handled by the machine, the final judgment—the nuanced “gut feel” that defines commercial lending—remains with the experienced banker.

Cloud-native architecture is also becoming the standard. In years past, banks were hesitant to move sensitive financial data off-premise, but the security and scalability of the cloud have won the day. A cloud-based commercial loan origination software allows for seamless remote work, enabling a relationship manager to pull up a client’s entire file on a tablet while sitting in the client’s office. This mobility creates a more collaborative and responsive relationship, which is ultimately what commercial borrowers value most.

Final Thoughts on Digital Transformation

Investing in commercial loan origination software is more than just a technical upgrade; it is a commitment to a different way of doing business. It is about moving from a world of “what happened” to a world of “what is happening now.” By removing the friction from the lending process, institutions can focus their energy where it belongs: on building relationships and helping businesses grow. The lenders who embrace this technology will find themselves with lower costs, happier employees, and a significantly more loyal customer base.

Ultimately, the goal of any commercial loan origination software is to make the complex appear simple. When the technology works as it should, the borrower sees a fast, transparent process, the underwriter feels empowered by accurate data, and the institution stays protected through consistent compliance. In a world where capital is a commodity, the experience you provide through your technology is the only thing that truly sets you apart.