The Medical Imaging Workstations Market is experiencing substantial growth, driven by the increasing demand for advanced imaging technologies and the need for efficient diagnostic solutions in healthcare. Medical imaging workstations play a crucial role in processing and analyzing imaging data, enabling healthcare professionals to make accurate diagnoses and treatment decisions.

Download Free Sample Report: https://www.snsinsider.com/sample-request/2085

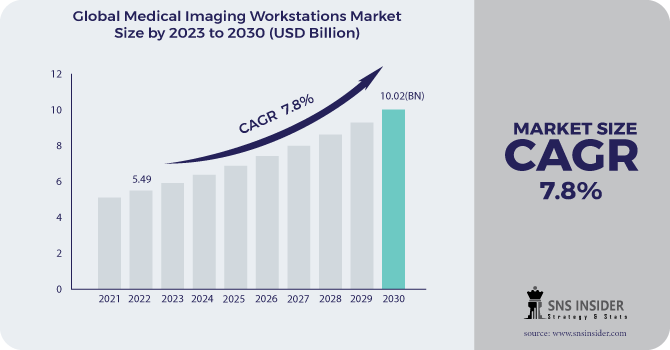

Market Overview:

The Medical Imaging Workstations Market was valued at USD 5.49 billion in 2022 and is projected to reach USD 10.02 billion by 2030, growing at a compound annual growth rate (CAGR) of 7.8% over the forecast period from 2023 to 2030.

Key Growth Drivers:

- Advancements in Imaging Technology: Continuous innovations in imaging modalities such as MRI, CT, and PET scanners are driving the demand for advanced workstations capable of handling complex data and providing high-resolution images.

- Increasing Prevalence of Chronic Diseases: The rise in chronic conditions, including cancer, cardiovascular diseases, and neurological disorders, necessitates the use of advanced imaging workstations for accurate diagnosis and monitoring.

- Rising Demand for Early Diagnosis: The focus on early detection and preventive healthcare is boosting the adoption of sophisticated imaging solutions to identify diseases at an early stage.

- Technological Integration and AI: Integration of artificial intelligence (AI) and machine learning algorithms into imaging workstations enhances diagnostic accuracy and operational efficiency, driving market growth.

Market Segmentation:

- By Product Type:

- Standalone Workstations: Dedicated systems designed for specific imaging modalities, providing focused functionality and performance.

- Integrated Workstations: Systems that combine multiple imaging modalities and features into a single platform for comprehensive analysis and reporting.

- By Modality:

- MRI Workstations: Specialized for processing and analyzing MRI scans, providing detailed imaging and advanced diagnostic capabilities.

- CT Workstations: Designed for handling data from computed tomography scans, offering high-resolution imaging and 3D reconstruction features.

- PET Workstations: Focused on processing and analyzing positron emission tomography scans, crucial for oncology and neurology diagnostics.

- Ultrasound Workstations: Used for managing and interpreting ultrasound images, essential for various diagnostic and therapeutic applications.

- By End-User:

- Hospitals: Major users of medical imaging workstations for a wide range of diagnostic and imaging needs.

- Diagnostic Imaging Centers: Facilities specializing in imaging services, requiring advanced workstations for efficient and accurate image processing.

- Research Institutions: Utilize imaging workstations for research purposes, including studies on disease mechanisms and development of new imaging technologies.

- Academic and Training Institutions: Employ workstations for educational purposes and training of healthcare professionals in imaging techniques and technologies.

- By Region:

- North America: Dominates the market due to advanced healthcare infrastructure, high adoption rates of imaging technologies, and significant investments in medical imaging research.

- Europe: Exhibits strong growth driven by increasing healthcare expenditure, advancements in imaging technologies, and a growing focus on early disease detection.

- Asia-Pacific: Expected to witness significant growth due to rising healthcare investments, expanding healthcare facilities, and increasing demand for advanced imaging solutions.

- Latin America and Middle East & Africa: Emerging markets with growth potential as healthcare infrastructure improves and the need for advanced diagnostic solutions rises.

Key Players:

- GE Healthcare: Provides a range of medical imaging workstations with advanced features and integration capabilities.

- Siemens Healthineers: Known for its innovative imaging workstations and solutions across various modalities.

- Philips Healthcare: Offers advanced workstations with integrated features and AI-powered diagnostic tools.

- Canon Medical Systems: Specializes in imaging workstations for different modalities, focusing on high-performance and user-friendly solutions.

- Hologic, Inc.: Provides advanced imaging solutions and workstations for breast imaging and other diagnostic applications.

Challenges:

- High Costs: The initial investment and maintenance costs associated with advanced imaging workstations can be substantial, potentially limiting their adoption in smaller healthcare facilities.

- Technological Complexity: The integration of complex technologies and the need for regular updates can present challenges in terms of user training and system maintenance.

- Regulatory Compliance: Ensuring that imaging workstations meet regulatory standards and certifications can impact design and manufacturing processes.

Future Outlook:

The Medical Imaging Workstations Market is set for substantial growth, driven by technological advancements, increasing demand for early diagnosis, and the integration of AI into imaging systems. By 2030, the market is expected to reach USD 10.02 billion, presenting significant opportunities for innovation and market expansion.