If you have ever opened a bank account, taken a loan, or bought an insurance policy in India, you have gone through KYC (Know Your Customer) verification. What most people do not realize is that this process is quietly getting faster and simpler across the industry, largely because of something called a CKYC API. This article looks at what CKYC is, the problem it was built to solve, and how a CKYC API fits into modern financial onboarding.

The Problem: Repeating KYC at Every Institution

For years, every bank, NBFC, and insurer in India maintained its own separate KYC records. If a customer had already completed KYC with one bank, no other institution had any way of knowing this. So the same person ended up submitting the same PAN card, Aadhaar, and address proof again and again, every time they opened a new account or applied for a new financial product.

This created real friction for everyone involved:

- Customers had to repeat the same paperwork at every new institution, which made onboarding slow and frustrating.

- Financial institutions ended up with duplicate, inconsistent records for the same person across different systems.

- Regulators found it harder to maintain a clean, auditable trail of KYC compliance across the industry, since records were scattered and paper-heavy.

To solve this at a structural level, the Reserve Bank of India set up the Central KYC Registry (CKYC), maintained by CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest of India). The idea was straightforward: create one shared, secure registry where a customer’s KYC record lives once, and any regulated institution can access it with the customer’s consent, instead of asking them to redo the process.

The Solution: What is a CKYC API?

Setting up a central registry solved the duplication problem in theory, but institutions still needed a fast, reliable way to actually use it. Manually searching government portals or exchanging files over SFTP is exactly the kind of slow, manual process the registry was meant to move away from.

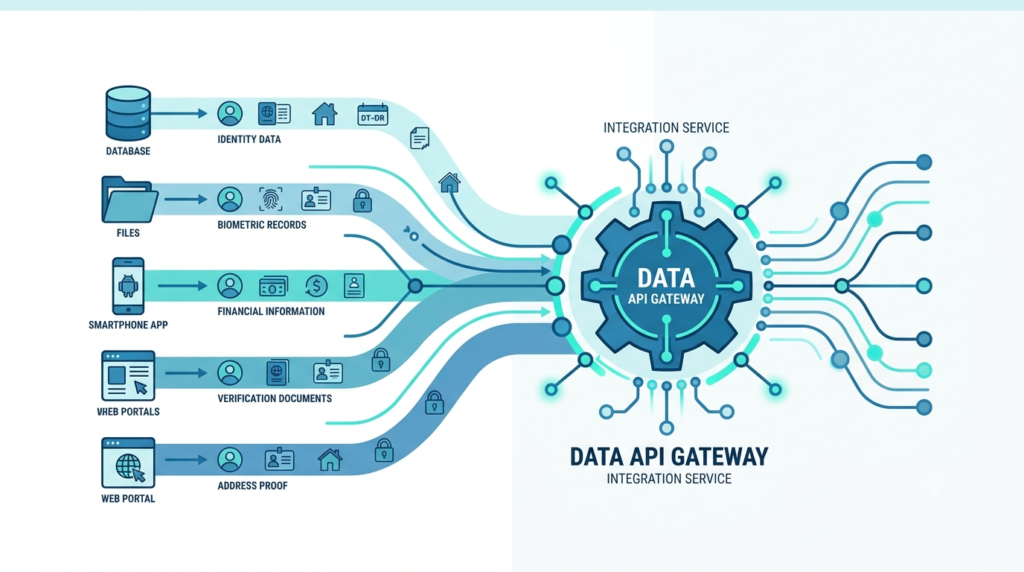

This is where a CKYC API comes in. It is the technical connection between a financial institution’s own onboarding system and the CERSAI CKYC registry, allowing that institution to search, fetch, upload, and update a customer’s KYC record programmatically, in real time, instead of through manual portal logins or file transfers.

In practice, this means a bank or NBFC’s onboarding software can check a customer’s KYC status, pull their verified details, or push a new record to the registry, all within the same flow a customer already sees on screen. Providers such as Surepass (surepass.io/ckyc-api) offer this as a ready-to-integrate API, which is a common approach for institutions that would rather plug into an existing, compliant system than build their own connection to CERSAI from scratch.

How the CKYC Process Typically Works

Regardless of which provider handles the integration, a CKYC workflow generally follows four steps:

- Search: The institution first checks whether a customer already has a CKYC record, using identifiers like PAN, Aadhaar, Driving Licence, or an existing CKYC number. This step alone prevents a large share of duplicate records from being created.

- Download: If a record exists, the verified KYC details can be retrieved directly, with the customer’s consent, instead of asking them to submit documents all over again.

- Upload: If no record exists yet, the new customer’s KYC details are formatted according to CERSAI’s requirements and submitted to create a fresh record.

- Update: When a customer’s address, contact information, or documents change later, their existing CKYC record can be updated rather than treated as a new case.

This four-step cycle covers the full life of a customer’s KYC record, from first onboarding through any future changes.

Why This Matters for the Industry

The shift toward CKYC APIs reflects a broader change in how compliance-heavy processes are being handled across Indian finance. A few benefits stand out:

- Faster onboarding, since existing customers do not need to resubmit documents that already exist in the registry.

- Fewer duplicate records, thanks to the built-in search step before any new record is created.

- Better compliance visibility, since API-based actions are logged and traceable, unlike manual, paper-based processes.

- Lower operational cost, as institutions no longer need large manual teams to manage paperwork and portal logins.

Banks, NBFCs, insurers, telecom companies, and fintechs are among the sectors that rely most heavily on this kind of infrastructure, simply because they onboard large numbers of customers on a regular basis.

In Summary

CKYC was built to fix a very practical, everyday problem: customers should not have to prove who they are over and over again at every financial institution they deal with. A CKYC API is what makes this shared registry usable in real onboarding systems, turning a good regulatory idea into something that actually works at the speed modern digital finance requires.

As more of India’s financial sector moves toward digital-first onboarding, CKYC APIs are likely to become a standard part of the infrastructure, much like PAN or Aadhaar verification already is.